[et_pb_section admin_label="Section" fullwidth="on" specialty="off"][et_pb_fullwidth_header admin_label="Fullwidth Header" title="Like 'em or hate 'em, we have to support initiatives" background_layout="light" text_orientation="left" header_fullscreen="off" header_scroll_down="off" parallax="off" parallax_method="off" content_orientation="center" image_orientation="center" custom_button_one="off" button_one_letter_spacing="0" button_one_use_icon="default" button_one_icon_placement="right" button_one_on_hover="on" button_one_letter_spacing_hover="0" custom_button_two="off" button_two_letter_spacing="0" button_two_use_icon="default" button_two_icon_placement="right" button_two_on_hover="on" button_two_letter_spacing_hover="0" subhead="October 2017"] [/et_pb_fullwidth_header][/et_pb_section][et_pb_section admin_label="section"][et_pb_row admin_label="row"][et_pb_column type="4_4"][et_pb_text admin_label="Text" background_layout="light" text_orientation="left" use_border_color="off" border_color="#ffffff" border_style="solid" saved_tabs="all"]

By David Schaeffer

[spacer height="03px"]

I’m just not sure anything will actually really happen

while the market continues to rage. At the end of the day,

if we could put our differences aside and focus on

common goals, we can actually get things done!

[spacer height="03px"]

However you look at the current President of United States, he is still our President. We can all agree that he is not articulate with the press, and not consistent in his public statements. At the end of the day, we need to get important stuff done. We voted for him, now we need to support him, so we can actually get what our country needs. We are like the crowd at the hometown game. We are the 12th man on the field. We can boo and hiss, or we can rally

for the common goal. I choose the latter.

[spacer height="03px"]

We need to FULLY employ our citizens and make up for over 12 years of zero wage growth. We need to fix the healthcare system for the 8% of Americans that need it. (Yup, the Affordable Care Act only affects 8% of the population. Seems like more, but no, just 8%.) We need to rebuild our country's infrastructure from the ground up. We need to CREATE American jobs. Which really means re-educating our workforce for important future-proof jobs, not service work. Modern work, like computer programming, is now called “coding”. The simple repetitive jobs are going away very quickly. Cashiers are being replaced by self-service checkouts. Wait staff at restaurants are aided by tableside tablets for drink refills and bill payment, and they too will soon become obsolete. Farming thousands of acres of America’s heartland are now plowed and harvested by remote-controlled, and self-driving equipment. Autonomous drones now survey miles of fence lines instead of cowboys. As for auto and home insurance sales, 42% of this type of insurance is purchased online without the need for human salespeople. Chatbots (artificially intelligent robots) are the first responders for most major companies when a consumer initiates an online chat. The Washington Post published a great many stories created autonomously by artificially intelligent software programs…not human journalists!

[spacer height="03px"]

If the last paragraph was completely foreign, I’m sorry. Today is different from any time in our past. Technology is progressing extremely fast. Today’s startup companies may follow a path unheard of to business leaders of the past. They may NEVER make a profit, on purpose!

[spacer height="03px"]

Our President is from the old school. Back in the days of Vanderbilt and Rockefeller, there was a term called “Robber Barron”. This is from a period of time when our country was growing at a pace so quickly, the world took notice as the United States became the most productive country on our planet. In those days, there was a similar disparity between rich and poor. The rich got richer and the poor…well, stayed poor.

[spacer height="03px"]

While the stock market is raging, 103 months without a significant decline, we still have very little inflation. Wage growth shows signs of improvement, but there is little growth in our tax base or bond interest rates.

[spacer height="03px"]

To fund public projects, the government needs to write a check, or issue a bond to fund the project. Since most state and local governments are not sitting on any excess money, issuing a bond is the only alternative. Hmmm,

[spacer height="03px"]

bonds are currently paying 1% to 2% with short term maturities. To get a 5% tax-free municipal bond, it won't mature until 2050. So… we sit and wait.

[spacer height="03px"]

I’m just not sure anything will actually really happen while the market continues to rage. At the end of the day, if we could put our differences aside and focus on common goals, we can actually get things done!

[/et_pb_text][et_pb_image admin_label="Image" src="https://americanretirementadvisors.com/wp-content/uploads/2017/09/Featured-story-1.jpg" show_in_lightbox="off" url_new_window="off" use_overlay="off" animation="left" sticky="off" align="left" max_width="250px" force_fullwidth="off" always_center_on_mobile="on" use_border_color="off" border_color="#ffffff" border_style="solid"] [/et_pb_image][/et_pb_column][/et_pb_row][/et_pb_section]

Financial Tip September 2017

[et_pb_section admin_label="Section" fullwidth="on" specialty="off"][et_pb_fullwidth_header admin_label="Fullwidth Header" title="Financial Tip" background_layout="light" text_orientation="left" header_fullscreen="off" header_scroll_down="off" parallax="off" parallax_method="off" content_orientation="center" image_orientation="center" custom_button_one="off" button_one_letter_spacing="0" button_one_use_icon="default" button_one_icon_placement="right" button_one_on_hover="on" button_one_letter_spacing_hover="0" custom_button_two="off" button_two_letter_spacing="0" button_two_use_icon="default" button_two_icon_placement="right" button_two_on_hover="on" button_two_letter_spacing_hover="0" subhead="September 2017"] [/et_pb_fullwidth_header][/et_pb_section][et_pb_section admin_label="section"][et_pb_row admin_label="row"][et_pb_column type="4_4"][et_pb_text admin_label="Text" background_layout="light" text_orientation="left" use_border_color="off" border_color="#ffffff" border_style="solid" saved_tabs="all"]

It’s Your Life.

[spacer height="03px"]

By Nancy Monaco-Ball

[spacer height="03px"]

“Life insurance is a waste of money.” That lady on TV says, “Only buy term. Whole-life is too expensive”, etc…

[spacer height="03px"]

We have heard every line out there regarding life insurance and I would agree all the above statements are true for someone. The problem is… are you sure it is for you?

[spacer height="05px"]

If you have ever sat down with any of our advisors, chances are you have heard one of us say there is no perfect financial tool. If there was a perfect financial tool, we would all have our money in it and live on a beach in Bora Bora, instead of Arizona in September. The key to any successful tool in retirement is education, and how those tools fit into a comprehensive retirement plan.

[spacer height="05px"]

Permanent life insurance should be considered a foundational element of any solid retirement plan, if your family is depending upon your retirement income, and you have not yet saved enough to live off dividends. The majority of the time we focus on our clients who are nearing retirement, and we constantly hear “We wish we would have come to see you 10 to 15 years ago”.

[spacer height="05px"]

When properly structured, permanent life insurance can provide tax-deferred growth, tax-free cash flow, and a tax-free death benefit. One of the biggest frustrations our clients have is their tax rate, once they retire. Most people assume their tax rate is lower, however, the majority of our clients see no decrease, and many times their taxes actually increase. Additionally, there are no RMDs with the cash value accumulated inside permanent life insurance. (IRS required minimum distributions or penalties for taking money out before age 59 ½.)

[spacer height="05px"]

How would you like to get $42,000 a year in tax-free income from age 66 to 85? By paying $12,000 for 16 years, from age 45 to 60, you may add tax-free income to your retirement plan. Maybe you, your children, or grandchildren have an old 401k that can be used to generate tax-free income in retirement but no one has ever explained the benefits.

[spacer height="05px"]

Permanent Life Insurance as an asset is not suitable for all, but like a wise man once told me, “you don’t know what you don’t know” and I definitely wouldn’t want to miss out on knowing how to get tax-free retirement income.

[spacer height="10px"]

This is a hypothetical illustration and is intended to show how assumptions affect the accumulation value and death benefit and it may not be used to project or predict dividend or interest credited results. Assumptions include a hypothetical interest rate, current mortality charges, and current expenses. The actual accumulation value and death benefit will vary based on a number of factors including the amount of dividend

or interest credited.

[/et_pb_text][et_pb_image admin_label="Image" src="https://americanretirementadvisors.com/wp-content/uploads/2017/09/Slide6.png" show_in_lightbox="off" url_new_window="off" use_overlay="off" animation="left" sticky="off" align="left" max_width="250px" force_fullwidth="off" always_center_on_mobile="on" use_border_color="off" border_color="#ffffff" border_style="solid"] [/et_pb_image][/et_pb_column][/et_pb_row][/et_pb_section]

Health Tip September 2017

[et_pb_section admin_label="Section" fullwidth="on" specialty="off"][et_pb_fullwidth_header admin_label="Fullwidth Header" title="Health Tip" background_layout="light" text_orientation="left" header_fullscreen="off" header_scroll_down="off" parallax="off" parallax_method="off" content_orientation="center" image_orientation="center" custom_button_one="off" button_one_letter_spacing="0" button_one_use_icon="default" button_one_icon_placement="right" button_one_on_hover="on" button_one_letter_spacing_hover="0" custom_button_two="off" button_two_letter_spacing="0" button_two_use_icon="default" button_two_icon_placement="right" button_two_on_hover="on" button_two_letter_spacing_hover="0" subhead="September 2017"] [/et_pb_fullwidth_header][/et_pb_section][et_pb_section admin_label="section"][et_pb_row admin_label="row"][et_pb_column type="4_4"][et_pb_text admin_label="Text" background_layout="light" text_orientation="left" use_border_color="off" border_color="#ffffff" border_style="solid" saved_tabs="all"]

Heat Exhaustion!!!

[spacer height="03px"]

By Sharon Cobert-Groves

[spacer height="05px"]

How sweet the summertime is!

[spacer height="05px"]

We get to enjoy various outdoor activities and events; experience the many joys of nature; and travel near and far to exchange love, and celebrate family reunions.

[spacer height="05px"]

Not so fast! Summer is not over yet. Here in Arizona the heat can last well into October. So we all need to be aware of possible “heat exhaustion” in both ourselves and our pets. First and foremost….never, ever leave a child, person or pet in a car! Second rule: Follow the first rule!

[spacer height="05px"]

Heat exhaustion can develop after several days of exposure to high temperatures during which a person either doesn’t drink enough fluids, or doesn’t replace enough of the fluid he or she loses because of the hot weather. It is milder than heat stroke. People at increased risk of heat exhaustion include the elderly, those with hypertension (high blood pressure), people who are overweight, children under 4 years old, and those who work or exercise in a hot environment.

[spacer height="05px"]

Warning Signs:

-heavy sweating -paleness -muscle cramps -tiredness -weakness -dizziness -headache -nausea

or vomiting -fainting -cool and moist skin -fast or weak pulse rate -fast and shallow breathing

[spacer height="05px"]

Important: If heat exhaustion is untreated, it may progress to heat stroke, which is much more serious. Therefore, if heat exhaustion symptoms get worse, or last more than one hour, immediate medical attention should be obtained.

[spacer height="05px"]

How do we treat possible heat exhaustion?

-drinking cool non-alcoholic beverages

-taking a cool shower, bath, or sponge bath

-being in an air-conditioned environment

-wearing lightweight clothing

-resting or a dip in the pool

[spacer height="05px"]

PLEASE, DON’T FORGET OUR FURRY FRIENDS. Remember, they have fur coats so Rule # 1: Never, ever, leave a pet in a parked car, even with the window cracked! This can be fatal!

[spacer height="05px"]

Remember, they have fur coats so Rule # 1: Never, ever, leave a pet in a parked car, even with the window cracked! This can be fatal!

[spacer height="05px"]

Dogs are not as efficient at releasing heat as we are; dog fur is great protection against the cold, but can be a problem in hot weather. This is because dogs eliminate heat by panting. When panting isn’t enough, their body temp rises. We may not be aware of the fact that a dog has become overheated until symptoms suddenly develop. A dog is overheated if his temperature is 103 degrees higher. A temperature of 109 °F (42.8 °C) is usually fatal. Heat stroke in dogs is a very serious condition and its onset can be sudden, escalating into an emergency situation in a matter of minutes potentially causing organ or brain damage and death. Dogs that are elderly, obese, or have a history of heart disease or seizures are more likely to suffer from heat strokes and may have a lower tolerance for increased heat.

[spacer height="05px"]

Some initial symptoms include:

[spacer height="05px"]

Some initial symptoms include:

-Excessive or loud panting

-Extreme thirst

-Frequent vomiting

-A bright red tongue and pale gums

-Skin around muzzle or neck doesn’t snap back when pinched

-Thick saliva

-Increased heart rate

[spacer height="05px"]

Worsening signs are:

-Increased difficulty breathing

-Gums that turn bright red, then blue or purple

-Weakness and/or fatigue

-Disorientation

-Collapse or coma

[spacer height="05px"]

What should you do?

Remove the dog from heat. Move indoors to an air-conditioned area. Restrict their activity until danger of heat stroke has passed. If you can, carry the dog rather than make him walk.

[spacer height="05px"]

Allow them to drink cool water. Not cold water. Cold or ice water will slow the dog’s cooling processes. Keep quantity small at first. Do NOT give animals human sports drinks. Unsalted chicken broth is acceptable if they won’t drink water. If the dog won’t drink on his own, wet his lips, gums, and tongue with water squeezed from a clean towel.

[spacer height="05px"]

Cool down the animal with water. If it’s coming from a hose, make sure water is not hot.

[spacer height="05px"]

Do not submerge dog under-water as he can lose temperature too quickly and lead to other complications. Place cool water-soaked towels between his back legs and in his armpits, or contact a veterinarian or take to the emergency clinic.

[spacer height="05px"]

Do not cover or confine the dog. You can wipe the dog down with cool, damp towels, but do not drape the towels over him, as they can trap in the dog’s body heat. do not place the dog in a closed crate that will hold the heat from his body in around his body.

[spacer height="05px"]

Together, we can all beat the heat. Pretty soon we’ll be back to our cooler sunny days and nights.

[/et_pb_text][et_pb_image admin_label="Image" src="https://americanretirementadvisors.com/wp-content/uploads/2017/09/Slide1.png" show_in_lightbox="off" url_new_window="off" use_overlay="off" animation="left" sticky="off" align="left" max_width="250px" force_fullwidth="off" always_center_on_mobile="on" use_border_color="off" border_color="#ffffff" border_style="solid"] [/et_pb_image][/et_pb_column][/et_pb_row][/et_pb_section]

Success Story September 2017

[et_pb_section admin_label="Section" fullwidth="on" specialty="off"][et_pb_fullwidth_header admin_label="Fullwidth Header" title="Success Story " background_layout="light" text_orientation="left" header_fullscreen="off" header_scroll_down="off" parallax="off" parallax_method="off" content_orientation="center" image_orientation="center" custom_button_one="off" button_one_letter_spacing="0" button_one_use_icon="default" button_one_icon_placement="right" button_one_on_hover="on" button_one_letter_spacing_hover="0" custom_button_two="off" button_two_letter_spacing="0" button_two_use_icon="default" button_two_icon_placement="right" button_two_on_hover="on" button_two_letter_spacing_hover="0" subhead="September 2017"] [/et_pb_fullwidth_header][/et_pb_section][et_pb_section admin_label="section"][et_pb_row admin_label="row"][et_pb_column type="4_4"][et_pb_text admin_label="Text" background_layout="light" text_orientation="left" use_border_color="off" border_color="#ffffff" border_style="solid" saved_tabs="all"]

Success Story of the Month

[spacer height="03px"]

By David S. Edge

[spacer height="03px"]

One phone call saved us lots of money!!!

[spacer height="03px"]

Gerry and JoAnn simply could not believe how many choices there are and were glad they had attended one of our many Medicare Workshops before deciding on their Medicare plan option.

[spacer height="03px"]

Months later, they were now getting ready to retire and were planning their exit strategies on how they were going to be debt-

free by paying off their house. They had decided to cash in one of their 401K accounts to accomplish their goal. They knew they would have to pay taxes on the withdrawal, but they really didn’t want a house payment anymore since they weren’t going to be working. Just before they transferred the money out of the account, they remembered something we told them; “don’t make any financial decisions without calling us first for a free review for possible financial implications”.

[spacer height="03px"]

They were excited about the possibility of being able to pay off their house, but what they did not realize was that they could

trigger unexpected expenses. By cashing in one of their 401K funds, their income would rise to over $170,000 on their joint tax return. They would then have to pay an increased amount for their Medicare Part B monthly premium. It increased from $134 each to $187.50 each. In a nutshell, they made and reported too much income and were now being penalized by Medicare. Additionally, they had to pay taxes on the cash they took out of the 401K!

[spacer height="03px"]

Cashing in your 401K to pay off your house isn’t always the best use of that money. What if you invested that money in a guaranteed principal account that pays you income while protecting your principal face amount of cash in the account? This way when you finish paying your house off with this income stream, you still have that principal amount of money to now generate income cash to pay your everyday living expenses! You also don’t have to pay Uncle Sam taxes on the withdrawn 401K money you cashed out, and you don’t run the risk of paying a higher Part B premium every month! It’s a win/win/win!

[spacer height="03px"]

After reviewing Gerry and JoAnn’s retirement funds and what they were currently invested in, we were able to make some improvements in their retirement cash flow! Now they could make their house payment without spending any of their principal money! When their house would be paid off in six more years, they would now have that income cash to spend!

[spacer height="03px"]

Everyone has their hopes and dreams of what they want their retirement years to become. Some want to be debt free, some want to travel, some want to remodel their home or downsize. Some folks just want to be financially worry-free.

[spacer height="03px"]

Whatever your retirement goals, come meet with

us to review what your possibilities are, and what they could be! Let’s meet and make a plan!!

[/et_pb_text][et_pb_image admin_label="Image" src="https://americanretirementadvisors.com/wp-content/uploads/2017/09/Slide5.png" show_in_lightbox="off" url_new_window="off" use_overlay="off" animation="left" sticky="off" align="left" max_width="250px" force_fullwidth="off" always_center_on_mobile="on" use_border_color="off" border_color="#ffffff" border_style="solid"] [/et_pb_image][/et_pb_column][/et_pb_row][/et_pb_section]

Featured Story 2 September 2017

[et_pb_section admin_label="Section" fullwidth="on" specialty="off"][et_pb_fullwidth_header admin_label="Fullwidth Header" title="Autumn Equinox" background_layout="light" text_orientation="left" header_fullscreen="off" header_scroll_down="off" parallax="off" parallax_method="off" content_orientation="center" image_orientation="center" custom_button_one="off" button_one_letter_spacing="0" button_one_use_icon="default" button_one_icon_placement="right" button_one_on_hover="on" button_one_letter_spacing_hover="0" custom_button_two="off" button_two_letter_spacing="0" button_two_use_icon="default" button_two_icon_placement="right" button_two_on_hover="on" button_two_letter_spacing_hover="0" subhead="September 2017"] [/et_pb_fullwidth_header][/et_pb_section][et_pb_section admin_label="section"][et_pb_row admin_label="row"][et_pb_column type="4_4"][et_pb_text admin_label="Text" background_layout="light" text_orientation="left" use_border_color="off" border_color="#ffffff" border_style="solid" saved_tabs="all"]

Welcome Fall!

[spacer height="03px"]

Friday, September 22, 2017, is the first day of fall for the Northern Hemisphere. Some folks don’t understand exactly what this day is about on the celestial calendar, but just so you know….this date is when we have an equal day and night. The same amount of daylight and the same amount of darkness.

[spacer height="03px"]

So, as you’ve guessed, equinox means equal night. Another way this can be the equinox is by temperatures. As the days get shorter, the temperature gets cooler. While this is especially true of Arizona, there are other States that are already getting cold weather and even some possibility of snow!

[spacer height="03px"]

Other highlights of fall are the turning of the leaves. One of the old Farmer’s Almanac quotes is “autumn leaves are slow to fall, prepare for a colder winter.” While this may give us longer to enjoy the fall colors, it can also be a tad foreboding with the notion that we need to hunker down for some above-average cold.

[spacer height="03px"]

Fall is also a time where baseball is winding down and football is revving up! So sports fans get double the pleasure and some wives become football widows! While watching sports and becoming couch potatoes we tend to gain some weight. That’s not good as we head into the holiday season where we traditionally gain even more each year.

[spacer height="03px"]

Fall also celebrates Friday night high school football with bands, cheerleaders, hot cocoa, and hot dogs. The kids are seeing if they can fit into last year’s winter coats and finding the missing glove that makes a matching pair. How does that happen every year? College is relegated to Saturday games with the Pro games on Sunday. Football, Football, and more Football!!!!!!

[spacer height="03px"]

County Fairs kick into full swing with Blue Ribbons handed out for the best of whatever (you can fill in the blank). Entertainment, in general, gets better: better TV and better movies, as ratings and nomination events get closer.

[spacer height="03px"]

While Halloween is just around the corner, we groan as retail stores are already putting up Christmas decorations!

[spacer height="03px"]

We start to lose our summer tans, but for some of us, the beautiful weather means more pleasant golf games and, in general, spending more time outdoors for a walk or a bike ride. Pets are also happy that the sidewalks aren’t so hot on their paws and maybe, just maybe, they’ll stop shedding so much!

[spacer height="03px"]

So enjoy these last hot days and keep an eye on the weather gauge as the weather starts its slow decline into our most beautiful time of year here in Arizona!

[/et_pb_text][et_pb_image admin_label="Image" src="https://americanretirementadvisors.com/wp-content/uploads/2017/09/Featured-Story-Edge.png" show_in_lightbox="off" url_new_window="off" use_overlay="off" animation="left" sticky="off" align="left" max_width="250px" force_fullwidth="off" always_center_on_mobile="on" use_border_color="off" border_color="#ffffff" border_style="solid"] [/et_pb_image][/et_pb_column][/et_pb_row][/et_pb_section]

Why am I Me Sept 2017

[et_pb_section admin_label="Section" fullwidth="on" specialty="off"][et_pb_fullwidth_header admin_label="Fullwidth Header" title="Why am I Me?" background_layout="light" text_orientation="left" header_fullscreen="off" header_scroll_down="off" parallax="off" parallax_method="off" content_orientation="center" image_orientation="center" custom_button_one="off" button_one_letter_spacing="0" button_one_use_icon="default" button_one_icon_placement="right" button_one_on_hover="on" button_one_letter_spacing_hover="0" custom_button_two="off" button_two_letter_spacing="0" button_two_use_icon="default" button_two_icon_placement="right" button_two_on_hover="on" button_two_letter_spacing_hover="0" subhead="September 2017"] [/et_pb_fullwidth_header][/et_pb_section][et_pb_section admin_label="section"][et_pb_row admin_label="row"][et_pb_column type="4_4"][et_pb_text admin_label="Text" background_layout="light" text_orientation="left" use_border_color="off" border_color="#ffffff" border_style="solid" saved_tabs="all"]

Computer Education and Automation!

[spacer height="03px"]

I don’t know about you, but like many current middle-aged Americans, I grew up and went entirely through school with no exposure to computers whatsoever. Oh sure…. we had typing and writing class so we at least could be competent on a keyboard but, no computers. I remember being wowed by the first IBM Selectric typewriter. A speed-typing and self-correcting typewriter! It was an amazing machine but nothing compared to our current computer processing.

While attending university, I saw my first electronic calculator from Texas Instruments. The thing was the size of a shoe box but boy could it calculate! I was impressed! As the years passed, calculators got smaller and smaller until now they can be as small as a credit card or even just an app on your phone.

[spacer height="03px"]

I try to keep up with all the changes in our new computerized world, but being an “older” adult, I often call my daughter to ask computer questions. I usually get a roll of the eyes and an additional “Oh Daddy, you should know this by now”. Recently though, I must have really pulled a bone-head of a question because she told me I must have “I. D. ten T disease”. It took me a few seconds to figure out what she just told me but then I realized ID10T (spells IDIOT disease). Oh, the joys your children can bring you. After we had a good laugh, she assisted me with my current computer dilemma.

[spacer height="03px"]

Point is, that as we progress through time, it’s getting harder and harder to just keep up with changes in communication, TV, phones, computers, and all this electronic new age-jazz! It can hurt your brain just thinking about keeping pace with these new-fangled modifications! I recently purchased a new Apple2 watch and I feel like Dick Tracy in the old Sunday morning paper comics with his radio watch. What was once science fiction……. is now a reality! Keeping up is becoming a full-time occupation!

[spacer height="05px"]

Well guess what? Each year there are changes to Medicare health plans, prescription drug plans, wills, trusts, financial planning opportunities, life insurance, and annuities in the ever-changing landscape of your retirement years.

[/et_pb_text][et_pb_image admin_label="Image" src="https://americanretirementadvisors.com/wp-content/uploads/2017/09/Slide3.png" show_in_lightbox="off" url_new_window="off" use_overlay="off" animation="left" sticky="off" align="left" max_width="250px" force_fullwidth="off" always_center_on_mobile="on" use_border_color="off" border_color="#ffffff" border_style="solid"] [/et_pb_image][/et_pb_column][/et_pb_row][/et_pb_section]

Life Insurance Sept 2017

[et_pb_section admin_label="Section" fullwidth="on" specialty="off"][et_pb_fullwidth_header admin_label="Fullwidth Header" title="Finding the right Insurance for you" background_layout="light" text_orientation="left" header_fullscreen="off" header_scroll_down="off" parallax="off" parallax_method="off" content_orientation="center" image_orientation="center" custom_button_one="off" button_one_letter_spacing="0" button_one_use_icon="default" button_one_icon_placement="right" button_one_on_hover="on" button_one_letter_spacing_hover="0" custom_button_two="off" button_two_letter_spacing="0" button_two_use_icon="default" button_two_icon_placement="right" button_two_on_hover="on" button_two_letter_spacing_hover="0" subhead="September 2017"] [/et_pb_fullwidth_header][/et_pb_section][et_pb_section admin_label="section"][et_pb_row admin_label="row"][et_pb_column type="4_4"][et_pb_text admin_label="Text" background_layout="light" text_orientation="left" use_border_color="off" border_color="#ffffff" border_style="solid" saved_tabs="all"]

By Kris Sollenberger

[spacer height="07px"]

“Take a look at three types of

life insurance. There has to be an option that may work for you. Talk with your loved ones. Get your family covered.”

[spacer height="05px"]

Expert planners have said….. if you’re alive, you need life insurance. Most of us probably agree on this. Well then, what’s stopping us from just grabbing up any old insurance and going about our day. Well, life insurance is pretty darn complicated. There are so many different types, how in the heck are you to know which one is best for you. Let’s go over a few, and hopefully, you’ll have your answer when you’re finished. OK.

[spacer height="03px"]

TERM life insurance is the most popular of them all. Why? Well, that’s easy, it’s the cheapest. This type of life insurance is like renting insurance. You pick the amount of years you want to be covered, if you die during that period, your family is paid. If you don’t die, well then the insurance company gets to keep all your premiums (money).

Again, it’s the cheapest for a reason, folks; the good news is you’re still alive.

[spacer height="03px"]

The most common term insurance is level premium. This is where you pay the same amount throughout the life of your policy. Term insurance has an annual renewable or flexible duration option as well. The annual renewable is where you renew every year, each year the premiums get more expensive. The flexible duration is just where you can specify the exact term you need between 1-35 years. There is also “return of premium” term coverage. This is the only term coverage that gets any of your money back, and of course, it’s more expensive.

[spacer height="03px"]

UNIVERSAL life is certainly more complicated. There are more variants to Universal Life. The meat of this insurance is that you have the option of flexible premiums that can be adjusted based on life events. This insurance is permanent, and will not expire unless you want it to. This type of coverage is more expensive than a term for the simple reason it creates a cash value. You don’t just rent this coverage, you own it. You can also play the market with universal life policies.

Generally, this is a good insurance to get if you want to avoid inflation risk, earn extra money by playing the market, or want flexible options for premiums. You can even borrow from your universal life insurance if you have enough cash value built up. This type of coverage has many options: indexed, universal, survivorship, guaranteed, variable, and guaranteed variable. One of them may work for you, and we can find that together.

[spacer height="03px"]

WHOLE life is the granddaddy of them all. With whole life, you own this policy until one of four things happen: You die, you have your 120th birthday, you stop paying your premiums, or you cancel your policy entirely. Whole life insurance is guaranteed insurance as long as you keep paying your premiums. Now, this is the more expensive type of coverage, but it builds a cash value like universal. Like universal, there are many options for this type of coverage as well. You can even get a type of coverage called Guaranteed Issue, in which you are guaranteed a policy even without any underwriting or medical history. This is obviously more expensive than if you let them search your background and check your health, but heck, it’s an option. There truly is a policy for everyone. Other whole life policies include graded, participating, level (most common), and 10 pay/20 pay options.

These are all a bit more complicated.

[spacer height="03px"]

We can help!

[/et_pb_text][et_pb_image admin_label="Image" src="https://americanretirementadvisors.com/wp-content/uploads/2017/08/Life-insurance-1.png" show_in_lightbox="off" url_new_window="off" use_overlay="off" animation="left" sticky="off" align="left" max_width="250px" force_fullwidth="off" always_center_on_mobile="on" use_border_color="off" border_color="#ffffff" border_style="solid"] [/et_pb_image][/et_pb_column][/et_pb_row][/et_pb_section]

Featured Story Sept 2017

[et_pb_section admin_label="Section" fullwidth="on" specialty="off"][et_pb_fullwidth_header admin_label="Fullwidth Header" title="Gotta love the market" background_layout="light" text_orientation="left" header_fullscreen="off" header_scroll_down="off" parallax="off" parallax_method="off" content_orientation="center" image_orientation="center" custom_button_one="off" button_one_letter_spacing="0" button_one_use_icon="default" button_one_icon_placement="right" button_one_on_hover="on" button_one_letter_spacing_hover="0" custom_button_two="off" button_two_letter_spacing="0" button_two_use_icon="default" button_two_icon_placement="right" button_two_on_hover="on" button_two_letter_spacing_hover="0" subhead="September 2017"]

[/et_pb_fullwidth_header][/et_pb_section][et_pb_section admin_label="section"][et_pb_row admin_label="row"][et_pb_column type="4_4"][et_pb_text admin_label="Text" background_layout="light" text_orientation="left" use_border_color="off" border_color="#ffffff" border_style="solid" saved_tabs="all"]

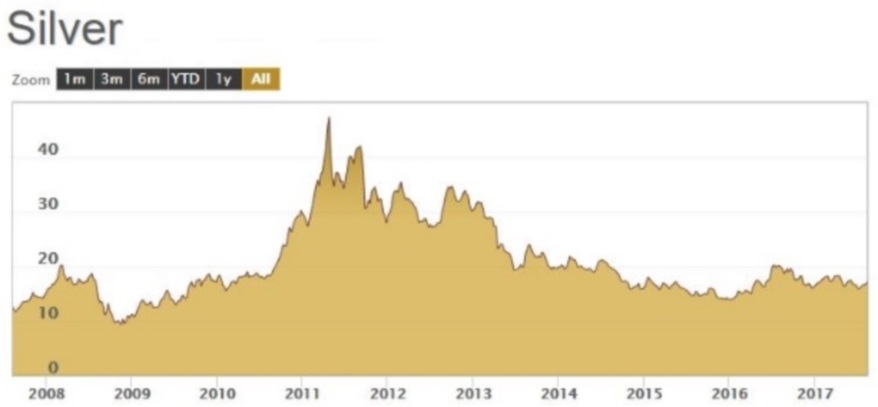

By David P Scheaffer

Up, Up, and Away (like TWA). Well, we all know what happened to TWA. It was great while it lasted! Most of our clients are nearing or in retirement. That usually means folks rely heavily on their savings for retirement. Wouldn’t it be great if we could all ride the UPs of the market and have a safety net if the market corrects?

[spacer height="03px"]

I’m not suggesting you run for the hills and put your savings into the mattress or heavy metals. Perhaps a mixed approach may be a good alternative to 100% of your savings exposed to the market. I like shiny metals.

If you visit our office, stop by, I keep a few bars around for fun. I’m not suggesting you buy them because they experience markets ups and downs as well.

[spacer height="03px"]

[spacer height="03px"]

When was the last time you had a Certified Financial Planner (CFP®) review your port-folio and provide a comprehensive overview of your life-long savings. The question was rhetorical, most folks have never met a CFP. My point… it’s your money!

[spacer height="03px"]

While the market is at an all-time high, stop to smell the roses. Take a look at carving off some of those gains and make sure you are protected from a market correction. (I hope you are making money in this market.) The last 3 times the market corrected it took over a decade for the recovery to get market values back to the same spot. Do you have 10 years to wait if the market drops again?

[spacer height="03px"]

The folks at the bank, credit union, and large brokerage firms are all nice people. They are doing the best they can with what they must work with. Their portfolios and choices are preselected to make sure the firm is protected against law suits. The offerings are vast in scope, but similar in that they mostly fluctuate to the market’s whims. Oh yeah, they also must make the firm residual income. While there is nothing wrong with making a living…

[spacer height="03px"]

What if what they are doing is not meeting your financial needs? What if the market drops 30%? What happens to your retirement income? My guess is it will drop as well, or you will need to dip into your principal to make ends meet. What happens next? Will you run out of money? It happened to millions of folks in the last market correction in 2007. Those retirees had to go back to work or, worse, sell their homes and move in with their kids.

[spacer height="03px"]

It doesn’t have to be that way. Hundreds of our clients weathered the last BIG financial storms with little or no change to their retirement income. We reveal how we do what we do. We keep no secrets. In fact, we share how we make decisions in your best interest, as well as how and what we get paid in the process. Did I mention we made our clients money in the last market correction?

[/et_pb_text][et_pb_image admin_label="Image" src="https://americanretirementadvisors.com/wp-content/uploads/2017/09/Slide2.png" show_in_lightbox="off" url_new_window="off" use_overlay="off" animation="left" sticky="off" align="left" max_width="250px" force_fullwidth="off" always_center_on_mobile="on" use_border_color="off" border_color="#ffffff" border_style="solid"]

[/et_pb_image][/et_pb_column][/et_pb_row][/et_pb_section]

[spacer height="08px"]

Wow…close calls. We’ve all had a few of these in our lives. There were some that were serious and others, not such a big deal. But a close call is a close call.

[spacer height="05px"]

Zooming down the freeway and you come upon an unmarked police car and you know your speeding….They don’t come after you and you have a sigh of relief. You think you just lucked out but it had your blood pressure up for a few minutes, didn’t it? You think to yourself, slow down, you just dodged a speeding ticket!

[spacer height="05px"]

Other times it was a more serious one, with maybe some surgery or a medical test on an uncertain lump on your body. The result was negative but…. it had you worried, didn’t it?

[spacer height="05px"]

Other times you’re shouting at the TV while watching a sporting event and you can’t get over how the umpire made such a bad ruling on a runner crossing home plate, or maybe the team was just short of a 1st down? That close call got you agitated but in reality… no harm, no foul, as far as consequences to you personally.

[spacer height="05px"]

I know I’ve had too many close calls to remember. There was a time in my young life where I was an apprentice carpenter on a house building crew and fell off a third story building and, luckily, landed in a pile of sand. I had a few bruises but it was an eye-opener, considering the possibility of a real injury had I landed on the concrete drive only a few feet away. That was luck.

[spacer height="05px"]

My daughter, while driving back to university one weekend, hit some black ice and caused a wreck that totaled her car. She walked away without a scratch; thankfully, she was wearing a seatbelt and it saved her life. People said she was lucky, I say luck had nothing to do with it. She was trained by her dad to always wear her seatbelt. She was prepared for her close call.

[spacer height="05px"]

These incidents have an impact on our lives. Maybe the result of one or more, causes us to be more careful when going about our lives. Maybe it changes our perception on a process or way of performing interactions. Maybe it wasn’t you but a close friend or relative that had the close call. Point is…. close calls change us. It can make us avoid those situations in the future as the ultimate deterrence to repeat that dangerous situation.

[spacer height="05px"]

What were some of your close calls? Can you remember what, when, and where it happened? Did the incident change the way you did something going forward? Who was with you? What were the details? Can you remember how it changed you?

[spacer height="05px"]

Don’t have close calls when you can prepare for them in advance and avoid them all together. Get the training, knowledge, and preparation from someone you trust and who is an expert on the topic. So if you need medical and drug plan advice, Long-Term Care coverage, Wills, Trusts, or financial retirement planning, it’s all at your fingertips by just giving us a call.

[spacer height="05px"]

Got your Will or Trust in order? When is the last time you updated it? Do you have your Power Of Attorney for health and financial matters written? Do you need Long-Term Care coverage or Life Insurance? Travel Insurance? When is the last time you reviewed your health coverage? Got questions? Give us a call, we are here to help!

[spacer height="05px"]

Don’t wait until it’s too late. It’s the old “an ounce of prevention is worth a pound of cure”.

[spacer height="10px"]

When discussing building retirement financial plans, inevitably the word “Annuities” comes up in the conversation. Folks react with pleasure or we get an “oh no, not annuities “.

[spacer height="05px"]

Many times we try to explain that annuities are just a tool that can play a part in your retirement. The first question I always ask is which type of annuity are you talking about? This often gets me a blank stare as most folks don’t realize there are different types of annuities and that they all have different purposes.

[spacer height="05px"]

I use the example that most people don’t realize that their Social Security check they get every month is a type of annuity. You paid into the system and the system is going to give you a paycheck for life. With the different types of Annuities, you just need to determine which format will fit your needs.

[spacer height="05px"]

Fixed Annuity is when you deposit money with an insurance company for a period of time of 1-20 years. The principle is fully insured and your interest rate is guaranteed.At the end of the time of the contract, your principal is returned. This one works like a CD at a bank, but often these Annuities outperform Bank rates of interest.

[spacer height="05px"]

Immediate Annuity is when you give money to an insurance company and the funds are no longer yours. In return, they promise a guaranteed income for you, or you and your spouse, for a period of time, which can be both of your lifetimes.

[spacer height="05px"]

Variable Annuity is usually the bad boy of “Annuities.”Your principal is at risk and there are fees in the 2-4% range that you pay even if the Variable Annuity losses principal. This Annuity is directly invested in sub accounts similar to mutual funds. The value of your account varies up and down with the market. This is where there are risks of losing your principal.

[spacer height="05px"]

If you have an errant adult child, these types of products can be controlled from the grave and allow you to plan how your child can be taken care of financially even after you're gone. This is especially valuable with a disabled spouse or child.

[spacer height="05px"]

So Annuities? Good or Bad? No such thing as they each have their uses. You need to view them as tools in your retirement tool box of products to take care of certain areas of your retirement financial well-being. These are just some of the ways you can achieve a well-balanced retirement plan.

[spacer height="05px"]

Need help in finding out if these are right for you and will solve an income issue as part of your financial plan? Call Us! We're here to help!

[/et_pb_text][et_pb_image admin_label="Image" src="https://americanretirementadvisors.com/wp-content/uploads/2017/08/Financial.png" show_in_lightbox="off" url_new_window="off" use_overlay="off" animation="left" sticky="off" align="left" max_width="250px" force_fullwidth="off" always_center_on_mobile="on" use_border_color="off" border_color="#ffffff" border_style="solid"] [/et_pb_image][/et_pb_column][/et_pb_row][/et_pb_section]

[spacer height="03px"]

When was the last time you had a Certified Financial Planner (CFP®) review your port-folio and provide a comprehensive overview of your life-long savings. The question was rhetorical, most folks have never met a CFP. My point… it’s your money!

[spacer height="03px"]

While the market is at an all-time high, stop to smell the roses. Take a look at carving off some of those gains and make sure you are protected from a market correction. (I hope you are making money in this market.) The last 3 times the market corrected it took over a decade for the recovery to get market values back to the same spot. Do you have 10 years to wait if the market drops again?

[spacer height="03px"]

The folks at the bank, credit union, and large brokerage firms are all nice people. They are doing the best they can with what they must work with. Their portfolios and choices are preselected to make sure the firm is protected against law suits. The offerings are vast in scope, but similar in that they mostly fluctuate to the market’s whims. Oh yeah, they also must make the firm residual income. While there is nothing wrong with making a living…

[spacer height="03px"]

What if what they are doing is not meeting your financial needs? What if the market drops 30%? What happens to your retirement income? My guess is it will drop as well, or you will need to dip into your principal to make ends meet. What happens next? Will you run out of money? It happened to millions of folks in the last market correction in 2007. Those retirees had to go back to work or, worse, sell their homes and move in with their kids.

[spacer height="03px"]

It doesn’t have to be that way. Hundreds of our clients weathered the last BIG financial storms with little or no change to their retirement income. We reveal how we do what we do. We keep no secrets. In fact, we share how we make decisions in your best interest, as well as how and what we get paid in the process. Did I mention we made our clients money in the last market correction?

[/et_pb_text][et_pb_image admin_label="Image" src="https://americanretirementadvisors.com/wp-content/uploads/2017/09/Slide2.png" show_in_lightbox="off" url_new_window="off" use_overlay="off" animation="left" sticky="off" align="left" max_width="250px" force_fullwidth="off" always_center_on_mobile="on" use_border_color="off" border_color="#ffffff" border_style="solid"]

[/et_pb_image][/et_pb_column][/et_pb_row][/et_pb_section]

[spacer height="03px"]

When was the last time you had a Certified Financial Planner (CFP®) review your port-folio and provide a comprehensive overview of your life-long savings. The question was rhetorical, most folks have never met a CFP. My point… it’s your money!

[spacer height="03px"]

While the market is at an all-time high, stop to smell the roses. Take a look at carving off some of those gains and make sure you are protected from a market correction. (I hope you are making money in this market.) The last 3 times the market corrected it took over a decade for the recovery to get market values back to the same spot. Do you have 10 years to wait if the market drops again?

[spacer height="03px"]

The folks at the bank, credit union, and large brokerage firms are all nice people. They are doing the best they can with what they must work with. Their portfolios and choices are preselected to make sure the firm is protected against law suits. The offerings are vast in scope, but similar in that they mostly fluctuate to the market’s whims. Oh yeah, they also must make the firm residual income. While there is nothing wrong with making a living…

[spacer height="03px"]

What if what they are doing is not meeting your financial needs? What if the market drops 30%? What happens to your retirement income? My guess is it will drop as well, or you will need to dip into your principal to make ends meet. What happens next? Will you run out of money? It happened to millions of folks in the last market correction in 2007. Those retirees had to go back to work or, worse, sell their homes and move in with their kids.

[spacer height="03px"]

It doesn’t have to be that way. Hundreds of our clients weathered the last BIG financial storms with little or no change to their retirement income. We reveal how we do what we do. We keep no secrets. In fact, we share how we make decisions in your best interest, as well as how and what we get paid in the process. Did I mention we made our clients money in the last market correction?

[/et_pb_text][et_pb_image admin_label="Image" src="https://americanretirementadvisors.com/wp-content/uploads/2017/09/Slide2.png" show_in_lightbox="off" url_new_window="off" use_overlay="off" animation="left" sticky="off" align="left" max_width="250px" force_fullwidth="off" always_center_on_mobile="on" use_border_color="off" border_color="#ffffff" border_style="solid"]

[/et_pb_image][/et_pb_column][/et_pb_row][/et_pb_section]