Estate planning needs to be done properly – September 2022

Estate planning done improperly can be a family nightmare. Adding insult to injury is that when a loved one passes away, the executor or trustee is responsible for the estate and pays the final bills. This can include legal fees, court costs, and time delays. They also must settle disputes and ensure the estate is distributed according to the instructions left behind.

Often, the executor pays out of pocket for expenses, such as the funeral, travel costs, and celebration of life. Depending on family dynamics, this can lead to disagreements and even arguments regarding reimbursement. Interesting side note: Do you know who paid for the singer Prince's funeral? George Lopez did. Yup, the comedian and friend. Why? Because Prince's 4-million-dollar estate was tied up. They couldn't release any assets until they had a death certificate and legally settled the estate.

No one wants to talk about the end of their life. But prepared or not, it is still going to happen. And there will always be a cost associated with it, whether it's the simplest of cremations or a traditional funeral. The planning is for the family that carries on after you. Having a plan will give families peace of mind from the financial stress so they can focus on the hundreds of decisions that will need to be made.

Buying preneed directly from a funeral home can sometimes be a good option. Even choosing the details of your send-off will ensure that the family won't have to make or pay for those decisions. And the estate doesn't have to be settled to get to the funds.

Another option is a unique product from a life insurance company that doesn't require a death certificate because of the way it's set up. Why is that important, you ask? Well, depending on where you live, getting a death certificate could take up to a month or more. You can get this product up to age 100, and there are no health questions (yes, really).

Suppose the family needs liquid assets right away. You could gift the assets to your family now to avoid probate, court costs, and time delays. But now, the assets belong to the person you entrusted. It now belongs to them. That means that they can be sued for it. It can be divided in the case of a divorce —all kinds of ramifications of this method.

We still feel that you should consider all options; wills, trusts, quit claim deeds for real estate, etc. We can help you determine what may be the right strategy for you. No charge. We just want to help.

All of that said, we wish you a long, healthy, and happy life!

July tends to be weak – August 2022

Hi all! Again, I must start out by saying that I’m writing this article in mid-July. June was a roller coaster ride for the stock market but had a little bit of a budding rally here towards the end of the month. In a typical year, July isn't that bad of a month. You see the S&P 500 up 0.05% on average, going all the way back to 1950. But July is usually the weakest month of all the summer months. And in years where the S&P 500 is down 10% or more through June, well, we're looking at a tale of two markets here. The S&P is down almost half a percent and is positive less than 50% of the time.

The other thing that complicates the S&P 500 in the month of July, outside of being down through June, is that big elephant or donkey in the room known as the midterm elections. Typically speaking, the S&P 500 is weaker during midterm years than it is in non-midterm years. And when the market is down 10% or more, those losses are magnified in midterm years. If we look at the S&P 500 average monthly returns in midterm years, going all the way back to 1946, it just looks like garbage, basically, from June through September. July, you get a little bit of a bump compared to say June or August, but still not very good-looking. And you see just from July through September, a pretty mean selloff, but by October, we typically see the market rip

off those September lows through the end of the year. The scariest part of the year in midterm years is actually during the summer.

When you look historically at markets where the S&P has been down 10% or more through June, and in midterm years, the weakness is just much too strong to ignore. So, make sure you're taking precautions. You've got sell stops on your trades if you're a trader, or if you're a long-term investor, you might want to buy these dips, but knowing you're going to have to have a strong stomach for what could be a volatile month here in July. As I've been saying all year, the back half of 2022 should be very nice.

If you are just pulling your hair out and would like to turn it over to the pro’s to manage, we are here for you. Our team is on top of the changing market as well as positioning portions of our portfolios in products that are fully insured and have no fees but can also take advantage of potential market gains.

Give your American Retirement Advisor a call. We can help!

How about that stock market – July 2022

[et_pb_section fb_built="1" _builder_version="3.22"][et_pb_row _builder_version="3.25" background_size="initial" background_position="top_left" background_repeat="repeat"][et_pb_column type="4_4" _builder_version="3.25" custom_padding="|||" custom_padding__hover="|||"][et_pb_text _builder_version="4.4.4" hover_enabled="0"] How about that stock market? Disclosure: I'm writing this article in June. At the end of 2021, we set out our projections for the stock market in 2022: 5,251 for the S&P 500 and 40,000 for the Dow. Those projections were based on our expectations for both profit growth in 2022 and the yield on the 10-year Treasury. At that time, given interest rates, the US stock market was still under our estimate of fair value. That is no longer true. Given the surge in long-term interest rates in 2022, the US stock market was now fairly valued for the first time in over a dozen years, dating back to the panic in 2008. During many of these past twelve years, with the US stock market well under fair value year after year, we often lifted our year-end forecast. But here we are in early June, and a vicious sell-off in the bond market has pushed the 10-year yield to 3.1%, much higher than the end of last year and above our 2.5% estimate. This higher yield makes a world of difference in how our model sees the stock market. Based on corporate earnings, we see the stock market as undervalued by roughly 20%. We think the outlook through year-end suggests a larger gain than normal when stocks are at fair value. First, some investors are already pricing in a recession for this year or early 2023. But we don't see a recession starting that soon. As the most pessimistic investors realize they were wrong, that adjustment should drive equities upward. It's a classic wall of worry that can help boost stocks, with bad news in the near term, already over-priced. All polls out there are signaling that there will be a red wave in November. This is not to say Republican wins are always good for equities; they're not, far from it. In the current political situation, a Republican Congress creates a divided government where the odds of tax hikes would be dead. In addition, the judicial branch is taking a tougher line on federal regulations. Put it all together, and we think there's a recipe for an equity rally into year-end, with the S&P 500 ending the year at 4,900 and the Dow at 39,000. However, assuming some modest increases in interest rates from here, such a rally would also put the stock market in overvalued territory. So, the rally we're projecting would be something for equity investors to enjoy but not a reason to become complacent. This means that you can't just "set it and forget it," as Ron Popeil used to say in his infomercials. Instead, you or an advisor that you trust, preferably a fiduciary, like we are, should be actively managing your assets to take advantage of the market's upward movement and weather the storms of the downward trends. We are here to help. Call us anytime [/et_pb_text][/et_pb_column][/et_pb_row][/et_pb_section]Is it hot yet? – June 2022

[et_pb_section fb_built="1" _builder_version="3.22"][et_pb_row _builder_version="3.25" background_size="initial" background_position="top_left" background_repeat="repeat"][et_pb_column type="4_4" _builder_version="3.25" custom_padding="|||" custom_padding__hover="|||"][et_pb_text _builder_version="4.4.4" hover_enabled="0" admin_label="Text"]Is it hot yet? Not as hot as the housing market! For this issue, I’m going to talk about finding extra money. If you’re a homeowner, you’re in luck.

My wife, Jacquie, has been a realtor for 20 years. We decided to move into our “forever” home by downsizing. We sold our 2-story and bought a slightly smaller 1-story house. We have no problem with stairs now, but who knows in the future. There is also less upkeep.

So how do you get money out of your house without creating more debt? Easy. The housing market is slowing down a little bit. A couple of hundred homes just hit the MLS in Vegas as I write this. We were and still are under inventoried. But the inventory is starting to fill back up. And prices are starting to come down. Don’t get me wrong; prices are still up there. But, if you sell a house that seems to be larger and emptier (i.e., the kids are grown and gone) than what you need in retirement, you now have a bunch of equity. How much, you ask? That depends on where you live and how long ago you bought it.

Look at it this way. If you sell the home you bought 10 years ago for, say, $350,000, owe $220,000, and now it appraises for (look on realtor.com) $700,000. You will pocket roughly $480,000. Take that equity to buy or put a down payment on your new smaller home with that $480,000.

If you still have a mortgage payment after that, it should be much smaller. The rates are low, but they are going up. On the other hand, if you sell a very expensive home, like my wife’s clients who keep moving to Vegas from California, you’re in for a treat. She had a client who sold their 1.5-million-dollar home in California and paid cash for a $600,000 home here. We now manage the remaining $900,000 for them. So now they have no mortgage payment and a nice comfortable income from our managed money portfolio. And no more stairs!

You don’t want to sell your house, but want extra income? You could always do a reverse mortgage. Back 10 years ago, I wouldn’t have advised that. But there are some good ones out there now. You just need a trustworthy broker who is honestly trying to help you. I have a couple that I have vetted that I introduce to my clients that could benefit from doing one. We don’t sell mortgages, but we can refer you to someone who can help.

Feel free to ask your American Retirement Advisor if any of these strategies interest you. We are here to help.

[/et_pb_text][/et_pb_column][/et_pb_row][/et_pb_section]Good money management -May2022

[et_pb_section fb_built="1" _builder_version="3.22"][et_pb_row _builder_version="3.25" background_size="initial" background_position="top_left" background_repeat="repeat"][et_pb_column type="4_4" _builder_version="3.25" custom_padding="|||" custom_padding__hover="|||"][et_pb_text _builder_version="4.4.4" hover_enabled="0"]Good money management is essential for all ages and stages of life. However, older adults' financial needs, spending, and saving patterns change. The thought of living on a fixed income can be scary.

Financial security and being prepared can come in many forms. At American Retirement Advisors, we assist folks with essential financial topics critical to success in retirement, including ways to ensure folks cash in on tax credits, deductions, and senior discounts. We also detail important ways to prepare for taking Social Security, building a retirement portfolio, and ensuring your estate is in order.

We target crucial aspects of financial planning, from claiming Social Security and retirement benefits to maximizing tax credits and deductions. We help you navigate your financial future, so you don't have to go it alone.

Having a trust, will, and estate plan in place helps protect you and your family from life's unexpected events. Of course, not all of these are needed for everyone, but we can help guide you to what makes sense for you.

If you're in the planning phase or already receiving Social Security, you're in good company! Approximately 65 million Americans receive Social Security payments monthly.

Understanding how Social Security fits into your finances is a powerful way to be prepared. Will Social Security cover all your financial retirement needs? There are several ways to understand how Social Security will fit into your overall financial goals and estimate your benefits. We'll take a closer look and try to make your choices clear. Yes, you do have choices.

According to the Federal Reserve Board's latest Survey of Consumer Finances, the median net worth of Americans aged 55 to 64 is $212,500. Your net worth is calculated by subtracting any liabilities, such as debt, from your assets. Your retirement accounts make up a portion of your assets. They also play a starring role in ensuring you can retire comfortably. Common accounts include 401(k), 403(b), 457(b), Thrift Savings Plan (TSP), Traditional & Roth IRA, and Pensions.

To make the most of these accounts and your retirement savings, we recommend that older adults first take advantage of company matches from their employers. Next, seniors should max out any tax-advantaged accounts, including 401(k)s, IRAs, or HSAs. Then, once you are over 59 and a half, it may make sense to sweep or roll the majority to your own IRA so that you are not confined to the list of mutual funds allowed in the plan and all the baked-in fees. Next, you can keep the 401(k) open to continue to deposit and get any matches. Finally, you can close the 401(k) and roll the rest to your IRA when you retire. Yes, we help folks do all of this too. As well as professionally manage the assets.

Well, that's all for now. Please feel free to call to schedule a no-cost financial assessment with your American Retirement Advisor. We are here to help.

[/et_pb_text][/et_pb_column][/et_pb_row][/et_pb_section]What you need to protect your assets – 2022

[et_pb_section fb_built="1" _builder_version="3.22"][et_pb_row _builder_version="3.25" background_size="initial" background_position="top_left" background_repeat="repeat"][et_pb_column type="4_4" _builder_version="3.25" custom_padding="|||" custom_padding__hover="|||"][et_pb_text _builder_version="4.4.4" hover_enabled="0"]We talk a lot about how to make money safely in our monthly financial tip. This month, I'd like to talk about what you need to protect your assets outside of what we do for you. Here at American Retirement Advisors, we exceed every required safeguard of your personal information. But I am guessing that you don't at home. Most folks don't do enough to safeguard their most precious asset - their identity. You probably have some protection on your credit cards. You may even have mortgage insurance. But do you have overall blanket protection that will cover all of that and more? Things like even your social media accounts. Your investment properties may not have a mortgage on them. Has your Social Security number been used without your consent? What about the passwords you use on hundreds of different online sites?

Well, there is a type of insurance that can protect against bad guys stealing your identity and spending all your money, and stealing your property. It's nothing that we sell here. But it is something that you should be aware of. If you're like me, you've heard advertisements for safeguarding products on television and radio. I enrolled in one of these plans a couple of years ago for myself and my wife.

I went online and reviewed all the top sellers at www.identityprotectionreview.com. This website does a pretty good comparative analysis of the main players. interestingly, one of the biggest advertisers came in fourth on the list, LifeLock. While I am not endorsing any companies, I went with number two on the list,

Identity Guard. It was a little less expensive than the number one rated product, and the only thing that I saw that it had that Identity Guard didn't have was anti-virus and Wi-Fi security. I already have those things with my Internet service provider, so I don't need them included. I did, however, pay a little bit more to have my real estate titles monitored. Number one on the list is a company called Aura. Both plans come with $1,000,000 identity theft insurance. With everything online, I feel that this is a must-have in this day and age. You need to select an identity plan that fits your needs.

Planning your Investments – 2022

[et_pb_section fb_built="1" _builder_version="3.22"][et_pb_row _builder_version="3.25" background_size="initial" background_position="top_left" background_repeat="repeat"][et_pb_column type="4_4" _builder_version="3.25" custom_padding="|||" custom_padding__hover="|||"][et_pb_text _builder_version="4.4.4"]Hello all, last year was a lesson in real-world economics. What happens when an unstoppable force of huge, unprecedented monetary and fiscal stimulus strikes the immovable object of supply shortages? Inflation!

When rising inflation started taking a bite out of everyone's budget earlier in the year, many predicted the demise of tech stocks. In some cases, we've seen technology stocks underperform relative to the market, such as the formerly high flying but not yet profitable names contained in some funds. But in many other cases, we've seen tech stocks soar.

We are trying to take advantage of uptrends in the market when it is safe to do so. Our custom-designed model portfolios are ever-changing. Our investment team runs thousands of algorithms daily to determine the best possible mix of investment choices. Yes, our investment team. Your plan starts with your advisor, then our plan designer, processors, and portfolio manager. The portfolio manager meets weekly with our advisory team and a built-in compliance officer to maintain the fiduciary standards. Our process goes like this:

Financial meeting one: You meet with your advisor to discuss your wants, goals, dreams, and ambitions. Then take a few minutes reviewing your assets and what you've been investing into this point. Your advisor will then hand the information off to one of our team members to build your plan to the specifications that meets your goals. They will then generate a binder containing all the recommendations in an easy-to-understand format.

Financial meeting two: You will be presented with your plan in this meeting. You may also meet your portfolio manager. We will go over your recommendations in detail. Once you feel comfortable with our suggestions, we will give you your binder to take home.

Financial meeting three: Now, after digesting the binder for a week or so, you can bring back any questions you didn't consider at our last meeting. By the end of this meeting, you can tell us how confident you feel about moving forward with some, all, or none of what we've presented. No worries if you choose not to move forward with any of what we've presented. You will not be charged for any of our meetings or the building of your plan. The plan is yours to keep. If you choose to move forward with some or all of the plan, then we will schedule meeting number 4.

[/et_pb_text][/et_pb_column][/et_pb_row][/et_pb_section]Strategic opportunities – 2021

[et_pb_section fb_built="1" _builder_version="3.22"][et_pb_row _builder_version="3.25" background_size="initial" background_position="top_left" background_repeat="repeat"][et_pb_column type="4_4" _builder_version="3.25" custom_padding="|||" custom_padding__hover="|||"][et_pb_text _builder_version="4.4.4"] Hello all! This month’s article is to share a strategic opportunity. Congress is going after the largest IRAs. The proposals in Congress might not become law, but our clients are hearing about them and want to hear from us on planning moves they could make to be better prepared. Congress has set its sights on mega-IRA balances, in large part due to the recent reports about a five billion dollar Roth IRA. But some of these proposals will impact many other clients with smaller individual retirement accounts and Roth IRAs. Now for the provisions that can affect many more of our clients. The proposals include an all-out ban on back-door Roth IRAs and mega-back-door Roth IRAs (from company plans), regardless of income level, so this means everyone. If you have been taking advantage of these provisions, especially the lucrative mega-back-door Roth, which can allow up to $58,000 this year to be contributed to after-tax plan accounts and converted to Roth IRAs, generally tax-free, this may be your last chance. So, make sure you get these done before year-end. The proposed ban would be effective after this year, like the other provisions mentioned above. If you placed funds in a traditional IRA to get the tax deduction and tax differed growth. The consensus is that, regardless of what we are hearing from DC, taxes will likely go up. Yes, even for the middle class. The Fed is spending unprecedented trillions, borrowing money from other countries and printing more. Add to that, closing loopholes like Roth conversions, it may be a good idea to move a portion of your Traditional IRAs to Roth IRAs while the tax brackets are relatively low and may not get back to where we are now for many years. This move is not the right decision for everyone. There are a lot of deciding factors. Is shifting assets from a Traditional IRA to a Roth IRA right for your planning? Our advisors can help. Give us a call at 877-220-1089 [/et_pb_text][/et_pb_column][/et_pb_row][/et_pb_section]Changes to Capital Gains Tax – 2021

[et_pb_section fb_built="1" _builder_version="3.22"][et_pb_row _builder_version="3.25" background_size="initial" background_position="top_left" background_repeat="repeat"][et_pb_column type="4_4" _builder_version="3.25" custom_padding="|||" custom_padding__hover="|||"][et_pb_text _builder_version="4.4.4" hover_enabled="0"]This month, I address an issue that is most likely going to get worse next year. I'm talking about Capital Gains Tax. House Democrats proposed a top federal rate of 25% on long-term capital gains by the House Ways and Means Committee. The maximum rate would be 28.8% when combined with a 3.8% surtax on net investment income. In 2022, it would kick in for single filers with taxable income over $400,000 and for married couples at $450,000, according to a committee aide. Now, I understand that this will affect a relatively small number of our clients. But, that said, it will affect some of you a lot.

This article is aimed at helping those of you that have highly appreciated assets and would like to sell said asset but feel that the capital gains tax would be prohibitive and eat up your gains. However, there is a possible solution.

The solution: A Charitable Remainder Trust (CRT) or Unitrust (also called a CRUT) is a gift of cash or other property to an irrevocable trust. The donor receives an income stream from the trust for a term of years or for life, and the named charity receives the remaining trust assets at the end of the trust term. But wait, that's not all. It's got a bit complex, but I will simplify as best I can.

Let's assume the asset is a building. You bought this building several years ago for 1 million. It's now worth 5 million. You create a CRUT and gift your building to that CRUT. You get a monster tax credit that you can use for 1 plus an additional 5 years, depending on when you need it. The CRUT then sells the building. Guess who is exempt from capital gains tax? Yup, the Charitable Trust! You then get to take income from the trust for the rest of your and your spouses' life.

When you die, the charities you named in the CRUT will receive the "remainder" of the assets in the trust. You can even create your own trust foundation and make your kids the trustees. They would then oversee dolling out the remainder to the charities of their choice. This can go on for decades after you pass. And the kids can take a fee for being the trustees.

Let's talk about the kids. You scored -the IRS lost (using their own rules)but the kids also may have lost. So, to make the kids whole, you can take a fraction of the income from the trust over the first 7 years and buy a Last to Die Life Insurance Policy to replace the 5 million. We would create another trust called an Irrevocable Life Ins Trust to buy the life policy. We do that to keep the death benefit and cash value outside of your estate for estate tax purposes because, let's face it, that probably will get worse too.

So, if this scenario fits you and your stock, real estate, precious metals, or any other highly appreciated asset, we are here to help. This is not something that most advisors out there know about or are experts at doing. We have worked with outside counsel uniquely versed in these strategies, and I have had experience creating these arrangements over the years. Before I joined American Retirement Advisors, companies like Wells Fargo Private Client Services and Morgan Stanley would call on me to build these plans for their clients. I was the resident expert for The Hartford and on loan to all of the major firms in Las Vegas. I am here to help.

[/et_pb_text][/et_pb_column][/et_pb_row][/et_pb_section]Our 4 cornerstone process – 2021

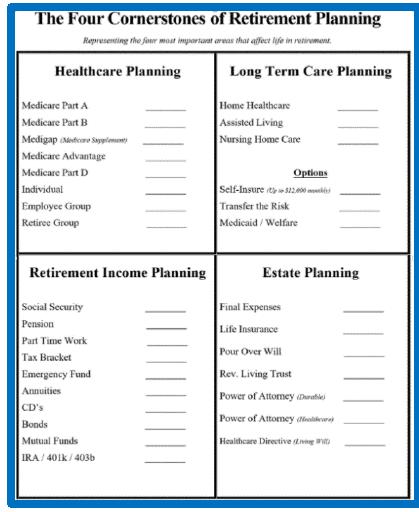

[et_pb_section fb_built="1" _builder_version="3.22"][et_pb_row _builder_version="3.25" background_size="initial" background_position="top_left" background_repeat="repeat"][et_pb_column type="4_4" _builder_version="3.25" custom_padding="|||" custom_padding__hover="|||"][et_pb_text _builder_version="4.4.4" hover_enabled="0"]Welcome to October. This month I thought I would go back to the core of what we all do here at American Retirement Advisors. Our firm is holistic in nature, which means that we help with the entirety of retirement planning. Not just insurance, or just Social Security, or just assets and income planning. The entire package. Let me explain our 4 Cornerstone process.

(Remember, if you only have three legs on a four legged chair, you're going to fall.) We start with a foundation of health Nothing else matters if you're not taking care of your health. So, first, we decide on healthcare coverage that fits your budget and lifestyle either group insurance from work or Medicare with a Supplement or an Advantage plan. As most of you know, we favor no one company or plan and present all available in your area.

Now, Long Term Care (LTC) planning is an insurance and financial hybrid for your holistic plan. On the one hand, it may be a health necessity. On the other, it can certainly drain your accounts quickly if it pays for a long term care facility, assisted living facility, or home health care. Of course, if you qualify f or Medicaid (qualifications differ by state), you won't need a LTC policy. But if your assets disqualify you for Medicaid for long term care, there are financial strategies that we may be able to deploy to help. *NOTE* You must set up these strategies before needing the care.

Retirement Income planning sets up the overall way you will live covering reoccurring bills for housing, utilities, food, and the like making sure that you can have the extras you want and not run out of money. We answer questions like: Should I pay off my house and cars? How much should I leave in the bank? Should I take my Social Security income early or wait? We build comprehensive retirement income plans and do not charge anything for the process because the planning is that important.

And finally, Estate planning . Whether you're of modest means or a Rockefeller, you need a plan. Are your wishes in writing? Do you need a will, a trust, a Power of Attorney, a living trust? Who gets your money who gets your s tuff when you die? Your house and cars? Your dog!? What if you don't die, but you can't care for yourself or speak for yourself? Who takes care of you, and does that individual know? Not fun to think about, but you need to. It's all part of our complimentary planning process.